HOME BUYING TIPS

BUYING WITH COWAN HOME TEAM

At Cowan Home Team we are among the top home buyer’s agents for Mesa county in the Western Slope area of Colorado. We are leading residential housing experts who will make sure to walk you through the entire home buying process, even if you’ve done it before. We buy and sell homes in the towns of Grand Junction, Clifton, Fruita, Fruitvale, Orchard Mesa and Loma in Western Slope Colorado. Thinking about relocating from Denver, Salt Lake City, or Las Vegas areas, contact us so we can help you find your next dream home!

As leading professionals in residential real estate as well as local experts, we can offer you real-world advice on how to make an offer, why you need a pre-approval, how to make a counter-offer and what the market is up or down. We will walk you through the closing process, help you understand what a clear title means, why it’s important to get a home inspection and a home warranty. We know you’ve got questions and this is the place to find many of the answers. Please call, email, or text and ask us anytime.

HOME BUYING GUIDE & F.A.Q.

HOME BUYING IS A PROCESS.

While there are many points along the way to buying your first home, buying a home is a process. Our job is to get you through that process as smoothly as possible.

We’ve drawn on our own experience and other reputable sources to try and break it all down into a 10-step guide to help you better understand what goes into buying your first home. You can read more about each step by clicking on it to expand the text:

You need to ask yourself some important questions:

Do you know what you want?

Whether you are a first-time home buyer or entering the marketplace as a repeat buyer, you need to ask why you want to buy. Are you planning to move to a new community due to a lifestyle change or is buying an option and not a requirement? What would you like in terms of real estate that you do not now have?

RELATED: How to Leap Those First-Time Buyer’s Hurdles

Do you have a purchasing timeframe?

Whatever your answers, the more you know about the real estate marketplace, the more likely you are to effectively define your goals. As an interesting exercise, it can be worthwhile to look at the questions above and to then discuss them in detail when meeting with us, your REALTORS®.

RELATED: Buying Your First Home? 3 Seasoned Tactics To Transform Into An Ultra Smart First Home Buyer

Do you have the money?

Homes and financing are closely intertwined. (Financing is the difference between the purchase price and the down payment, commonly referred to as debt or the mortgage.) The good news is that over the years new and innovative loan programs have evolved which require a 5 percent down payment or less.

In addition to a down payment, purchasers also need cash for closing costs (the final costs associated with finalizing the loan). Less money down means higher monthly mortgage payments, so most home buyers choose to buy with some cash up front.

As to closing costs, in markets where buyers have leverage, it may be possible to negotiate an offer for a home that requires the owner to pay some or all of your settlement expenses or closing costs. We’ll cover that when we meet and get closer to buying the home.

Is your financial house in order?

Those great loans with little or nothing down are not available to everyone: You need good credit. For at least one year prior to purchasing a home, you should assure that every credit card bill, rent check, car payment and other debt is paid in full and on time. Try to postpone major expenses like a new car, etc. So you don’t over-extend yourself with a new car payment AND a new house payment.

RELATED: Spring Cleaning Your Credit Report Before a Home Purchase

Who you choose matters.

Why is this important?

Buying and selling real estate is a complex matter. At first it might seem that by checking local picture books or online sites you could quickly find the right home at the right price.

But a basic rule in real estate is that all properties are unique. No two properties — even two identical models on the same street — are precisely and exactly alike. Homes differ and so do contract terms, financing options, inspection requirements and closing costs. Also, no two transactions are alike.

In this maze of forms, financing, inspections, marketing, pricing and negotiating, it makes sense to work with professionals who know the community and much more. Those professionals are the local REALTORS® who serve your area. Yes, that’s us.

RELATED: Why It Pays to Use a Buyer’s Agent

How do you choose?

In every community you’re likely to find a number of realty brokerages. Because there is heated competition, local REALTORS® must fight hard to succeed in your community. Not every REALTOR® works as hard to earn your business. More importantly, we fight hard for YOU during your home buying process; looking out for you, helping you avoid pitfalls, giving you sound advice along the way. And we have the experience to help you make the most informed decision.

RELATED: 10 Questions Buyers Should Ask Their Realtor

What should you expect when you work with a REALTOR®?

Once you select a REALTOR® you will want to establish a proper business relationship. You likely know that some REALTORS® represent sellers while others represent buyers. Each REALTOR® will explain the options available describe how he or she typically works with individuals and provide you with complete agency disclosures (the ins and outs of your relationship with the agent) as required in your state. When you select us to help you buy your home, we become a Buyer’s Agent – that means we represent YOU during the whole process.

What does it cost for us to be your agent? It costs you NOTHING. When we are your Buyer’s Agent, our commission is paid by the seller of the house you select to buy. It’s actually a pretty good deal for the buyer!

Once hired for the job, we will provide you with information detailing current market conditions, financing options and negotiating issues that might apply to a given situation. Remember: Because market conditions can change and the strategies that apply in one negotiation may be inappropriate in another,

this information should not be set in stone. During your time in the marketplace we will keep you updated and alert you to each step in the transaction process.

RELATED: The Goal for Choosing an Agent Can Be Summed Up in 4 Words

This is an important step that shouldn’t be saved for later.

You’re ready, you’ve asked us to be your agent, let’s go look at houses! But wait, there’s another important step before we all get in the car: Getting pre- approved for a loan. Why? Because you really need to understand just how much of a home you can afford BEFORE you start looking. That way, you won’t be disappointed way down the road AFTER you found the home of your dreams – only to find out you really can’t get a loan for that price.

Here’s a big reality in buying a home: Few people can buy a home for cash. According to the National Association of REALTORS® (NAR), nearly nine out of 10 buyers finance their purchase, which means that virtually all buyers — especially first-time purchasers — required a loan.

The real issue with real estate financing is not getting a loan (virtually anyone willing to pay lofty interest rates can find a mortgage). Instead, the idea is to get the loan that’s right for you — the mortgage with the lowest cost and best terms.

We routinely suggest that consumers start the mortgage process well before making an offer on a home. We have a number of lenders we can suggest to you. We and our clients have worked with them several times over the years. By meeting with lenders — either on the phone or face to face — and looking at loan options, you will find which programs best meet your needs and how much you can afford.

We also recommend pre-approvals for another reason: Offers require buyers to apply for financing within a given time period, in many cases, seven to 10 days. By meeting with loan officers in advance and identifying mortgage programs, it won’t be necessary to quickly find a lender, check credit, and rush into a financing decision that may not be the best option.

What is pre-approval?

“Pre-approval” means you have met with a loan officer, your credit files have been reviewed and the loan officer believes you can readily qualify for a given loan amount with one or more specific mortgage programs. Based on this information, the lender will provide a pre-approval letter, which shows your borrowing power. You can shop around with as many lenders as you like to get a pre-approval letter. If you are shopping loans, you have a time period you can shop without affecting your credit. A lender can give you advice on this.

Although not a final loan commitment, the pre-approval letter will be submitted to the seller’s agent when we do make an offer on a home. In fact, it’s a MUST to furnish this along with the offer contract. It demonstrates your financial strength and shows that you have the ability to go through with a purchase. This information is important to owners since they do not want to accept an offer that is likely to fail because financing cannot be obtained. It keeps their home off the market for too long without this important element.

How do you get pre-approval?

It can start with an easy, 15-minute phone conversation with one of the lenders we can refer to you. We will only refer those with a history of offering competitive programs and delivering promised rates and terms.

The loan officer will carefully review your financial situation, including your credit report and other information. The lender will then suggest programs which most closely meet your needs.

Sometimes, during the pre-approval process, our clients learn they can’t quite qualify for a mortgage yet. This past January saw a bit of tightening on the loan qualification standards. Their credit score may not be as high as they thought. They may have a little more debt than is permitted under the standards. Even if this happens, it’s still better to know NOW, before the hours of home viewing begins. And the lenders we refer to you all have experience in giving you sound advice about how to get your financials in order to get you up to the standards needed to qualify for a mortgage. It’s an important step. DON’T skip this one!

Time to get in the car!

Congratulations! You called that lender and got a pre-approval letter for a mortgage! Now we’re ready to get in the car and look at homes together (the fun part). Here are some things to consider when deciding which homes to look at.

Millions of new and existing homes are sold each year. There’s no shortage of housing options, but with so many choices the challenge becomes finding the property which best meets your needs.

The housing market is complicated because the stock of homes for sale is always in flux. If it were possible to have a complete list of every home for sale at this very moment in a given community, such a list would become obsolete within seconds as new homes become available and properties now for sale are put under contract.

In effect, buyers are looking at a moving target in a marketplace that is never static. Because of this, it is important to know as much as possible about the choices in preferred markets, and the way to do that is by working closely with us, your agents, who have a good lay of the land.

RELATED: Online House Hunting The SAFE Way

What are you looking for?

A home is more than just a collection of bedrooms and bathrooms. Several properties — each with four bedrooms, three baths, and the same price — may well represent radically different designs, commuting distances, lot sizes, tax costs, interior dimensions, and exterior finishes.

Each of us is different and so it’s important to list the features and benefits you want in a home. Consider such things as pricing, location, size, amenities (extras such as a pool or extra-large kitchen) and design (one floor or two, colonial or modern, etc.).

Next, it’s important to consider your priorities. If you can’t get a home at your price with all the features you want, then what features are most important? For instance, would you trade fewer bedrooms for a larger kitchen? A longer commute for a bigger lot and lower cost?

Lastly, consider your needs in several years. If you’ll need a larger home, maybe now is the time to buy a bigger house rather than moving or expanding in the future. If you expect your income to increase, perhaps you should consider a more expensive home financed with a loan program where monthly payments increase in the future.

Where should you look?

All neighborhoods and communities have a special nature that gives them identity and value. One community may be well known for historic homes while another offers both suburban living as well as easy access to downtown office areas.

We have access to thousands of homes online. Our website, www.carolcowan.com is a fantastic place to begin. We have a search tool that draws information directly from the same multi-listing service all agents in the area use. It’s a terrific source for property information, online or off. Just click “Search” to get started!

Some like to search by looking at listings on the basis of location or price; others prefer to have us suggest properties; and many buyers prefer both approaches.

Regardless of your choice, it’s important to target your search. By using basic measures such as general location and affordability, you can refine your search and focus on homes that offer the most desirable features.

As a guide, you should maintain a file with information on each of the homes you like. You can print out listing pages from those you find while searching on our site and then make notes for each one — what you like, questions, nearby schools, data, etc.

We will often identify together a collection of homes to look at during a day. We’ll meet you there or pick you up to go look. Each house is secured with lockbox, with access only permitted to agents. This helps keep the home for sale secure from intruders. So, we accompany you to each house and help you identify good (and bad) features of each house. During this process make sure you let us know exactly what you like and do not like about each home. It helps us narrow in on just the right home for you. But don’t worry, we take keep a file for you of each home you’ve seen and take detailed notes to help us both remember what you did or didn’t like about each home you visit.

RELATED: Buy in the Right Location to Ensure Your Home’s Value

There’s no doubt that choosing a home is a big decision, and you want to do it right.

As a buyer, here’s what actually happens. A home has been placed on the market for which the seller has established an asking price as well as other terms. In effect, this is an offer. At this point, you have three choices: accept the seller’s offer and create a contract; reject it and not make an offer; or suggest different terms and make a counter-offer. If you choose this last option, the seller may accept, reject or make another counter-offer.

No aspect of the home buying process is more complex, personal or variable than bargaining between buyers and sellers. This is the point where the value of our experience as a REALTOR® is clearly evident because we know the community, we’ve seen numerous homes for sale, we know local values and we’ve spent years negotiating realty transactions.

Is it THE house?

A house is shelter, but a home is far more. It’s where you live, relax, entertain friends, raise families, and work. A home is where you spend much of your life, and so choosing a house is an enormous decision.

How do you know if a house is THE one? Probably the best approach is to look at as many homes as possible, something made easy by using the search tool on our site, where you can quickly and easily view huge numbers of homes, check prices, take video tours and view extensive neighborhood information. Once your choices have been narrowed, you can then contact us to find specific information and options.

Can you really afford it?

Remember STEP 2? – the pre-approval process? Getting pre-approved means you have a very good idea of how much you can borrow, what loan programs will most likely work best in your situation and how much home you can afford.

How reliable is a pre-approval? While pre-approval is not a loan commitment, it’s still necessary for lenders to check such items as appraisals and the latest credit reports. Despite fluctuating interest rates, pre- approval nonetheless provides a reasoned, careful analysis of what you can afford. After all, loan officers are routinely paid only when loans are originated. It doesn’t make much sense for loan officers to suggest high loan limits that later can’t be delivered.

During the Choosing A Home process we can also be a valued part of the team. We can help you evaluate the merits of one home versus others we’ve seen together. We can help you weigh the pros and cons of one you’ve selected. But, ultimately, this is YOUR choice. We’ll help all we can to help you make a confident, informed decision.

Financing is important; be informed!

Often the cost of real estate financing is routinely greater than the original purchase price of a home (after you include the interest on the loan and closing costs of finalizing the loan). Because financing is so important, buyers should have as much information as possible regarding mortgage options and costs.

Our web site has tools to help you find mortgage information as well as a loan calculator. We can also discuss financing options and recommend loan sources.

What kind of loan?

There are thousands of loans available out there from a variety of lenders, but in general, the mortgage you choose will likely be determined by at least several key factors:

• How much down? Loans with 5 percent down or less are available — in fact, loans from major

lenders with no money down are available only in certain areas. Or a HUD home that is $100 down but condition and availability make HUD homes very hard to obtain.

• If you place less than 20 percent down, lenders will want the mortgage guaranteed by an outside third party such as the Veterans Administration (VA), the Federal Housing Administration (FHA) or a private mortgage insurer (PMI, or private mortgage insurance, is required by lender to protect against any mortgage defaults). These are the loan programs most home buyers use. Millions of VA, FHA and PMI loans are generated each year.

• How’s your credit? The best rates and terms are only available to those with solid credit. To get the best loans, make a point of paying credit cards, installment payments, rent and mortgage bills in full and on time.

• Are you a first-time buyer? It might seem that “first-time buyer” means someone who has never owned property before, but under most state programs, the term refers to those who have not owned property within the past three years. State-backed first-timer programs often feature smaller down payments and below-market interest rates. For details, ask us for more information or one of the lenders we refer to you.

RELATED: Three Types of Mortgage Loans

RELATED: Using Gift Money To Help With Down Payment

How do you get a loan?

To obtain a loan you must complete a written loan application and provide supporting documentation. Specific documents include recent pay stubs, rental checks and tax returns for the past two or three years if you are self- employed. During the pre-qualification procedure, the loan officer will describe the type of paperwork required.

Where do you get a loan?

Mortgage financing can be obtained from mortgage bankers, mortgage brokers, savings and loan associations, mutual savings banks, commercial banks, credit unions, and insurance companies. More than likely, you’ll want to continue working with the lender we first referred you to during the pre-approval step. They already know you, your finances and have a feel for which program works best for you.

About closing costs

Closing costs are the costs associated with generating a mortgage loan. It’s something in addition to just the interest you’d pay over the life of the loan. There are a variety of fees and other costs mortgage lenders have to charge the borrower and your lender will give you a very detailed accounting of what those costs are BEFORE you actually buy the home or complete the loan process. In many cases we can negotiate and ask the seller to pay some or all of these costs for you as part of the offer you make to buy (see below). Just know there will always be some money you’ll need to come up with out of your own pocket to get a loan (such as a down payment, closing costs, inspections, etc.). Start planning your finances NOW for this.

There’s so many things to consider when it comes to making your offer.

REALTOR® groups, working with legal counsel, have developed forms that are appropriate for real estate transactions in specific communities. We are members of the National and Colorado Association of Realtors (GAR) which provides us with a complete set of standard forms to use in the home buying process. These documents include numerous sale conditions and their wording should be carefully reviewed to assure that they reflect the terms you want to offer. Don’t get overwhelmed by this. We can explain the general contracting process and we fill these forms out for you.

Using the standard forms above we put together a “contract” for your offer to buy a home, with a price and the terms under which you’re willing to buy it. It’s basically a “proposal” to buy the home. While much attention is spent on offering prices, a proposal to buy includes both the price and terms. These are extra things or conditions we want included in the contract. In some cases, terms can represent thousands of dollars in additional value for buyers — or additional costs. Terms are extremely important and we’ll carefully review these with you.

RELATED: Homebuyers Beware: Top 3 Things That Could Cause You to LOSE YOUR DEPOSIT!

How much?

You sometimes hear that the amount of your offer should be x percent below the seller’s asking price or y percent less than you’re really willing to pay. In practice, the offer depends on the basic laws of supply and demand: If many buyers are competing for homes, then sellers will likely get full-price offers and sometimes even more. If demand is weak, then offers below the asking price may be in order.

RELATED: What Happens When A Home Appraisal Falls Short?

How do you make an offer?

Here, you will complete and sign an offer (a contract) which we, the REALTOR®, will present to the owner and the owner’s representative. The offer also must be accompanied by “earnest money” from you (typically $1,000 or more, depending on the house). This money is used to demonstrate to the seller you are serious with your offer and you will be “earnestly” working through the loan and purchase process to actually buy it. Earnest money is held in a separate escrow account for safe-keeping until we actually complete the purchase of the house. That amount is credited to you at the closing meeting or refunded to you if you do not complete the purchase for a valid reason (more on all this a little later). Just know you should set aside about $1,000 or so for when you do find the house you want to make an offer on.

RELATED: How to Make an Offer on a House

Once you’ve made an offer or proposal to buy the house, the owner, in turn, may accept the offer, reject it or make a counter-offer.

Because counter-offers are common (any change in an offer can be considered a “counter-offer”), it’s important for you to remain in close contact with us® during the negotiation process so that any proposed changes can be quickly reviewed.

RELATED: Real Estate Tips: Real Estate Contracts and Pitfalls

What are inspections? How many inspections?

When you make an offer to buy a home we always recommend inspections of the home – or a closer look at it. A number of inspections are common in residential realty transactions. They include checks for termites, surveys to determine boundaries, appraisals to determine value for lenders, title reviews and general structural inspections.

RELATED: Do You Really Need a Pest Inspection When Buying a Home?

RELATED: Why Do I Need an HVAC Inspection?

Structural inspections are particularly important. During these examinations, an inspector comes to the property to determine if there are material physical defects and whether expensive repairs and replacements are likely to be required in the next few years. Such inspections for a single-family home often require three or four hours, and buyers should attend if possible This is an opportunity to examine the property’s mechanics and structure, ask questions and learn far more about the property than is possible with an informal walk-through. It’s similar to having a professional mechanic check out a used car before you buy it.

RELATED: Finding a Good Home Inspector

This can be a little intense for first-time home buyers because an inspector will often find some faults with the home you’ve fallen in love with. That’s because it’s the inspector’s JOB to find those faults. He or she is obliged to point them out to you so you know what you’re getting before you complete the purchase. But don’t get anxious during this phase: every single home has something that needs attention, repair or replacement. It doesn’t necessarily mean you shouldn’t go forward with the purchase. It just means there are things which may need attention.

When an inspection report shows issues with your intended home we can, through amendments to the contract, request the seller fix the issue as a condition for completing the sale. They may elect to do that. They may not. When they don’t agree, we’ll have an open discussion about whether it’s something you may want to fix yourself after you buy the home. Or it could be something you can live with. If the issue is a major concern, we have the opportunity to walk away from the deal and get your earnest money back.

RELATED: Trust, but Inspect – Why We Recommend Home Inspections

Wait… insurance?

Why do we need to talk about insurance when buying a home?

Well… no one would drive a car without insurance, so it figures that no homeowner should be without insurance. If you are getting a loan, the lender will require insurance.

The essential idea behind various forms of real estate insurance is to protect owners in the event of catastrophe. If something goes wrong, insurance can be the bargain of a lifetime.

What kind and how much?

There are various forms of insurance associated with home ownership, including these major types: Title insurance: Purchased with a one-time fee at closing, title insurance protects owners in the event that “title” to the property is found to be invalid. Title really just means the home is under the name of who actually, legally owns the home. If you are getting a FHA loan for more than 80% of the loan value, then the Mortgage Insurance Premium will be included in the loan.

Homeowners’ insurance: Homeowner’s insurance provides fire, theft and liability coverage. Homeowners’ policies are required by lenders and often cover a surprising number of items, including in some cases such property as wedding rings, furniture and home office equipment.

Flood insurance: Generally required in high-risk flood-prone areas, this insurance is issued by the federal government and provides as much as $250,000 in coverage for a single-family home plus $100,000 for contents. Local REALTORS® can explain which locations require such coverage.

Home warranties: With new homes, buyers want assurance that if something goes wrong after completion the builder will be there to make repairs. But what if the builder refuses to do the work or goes out of business?

Home warranties bought from third parties by home builders are generally designed to provide several forms of protection: workmanship for the first year, mechanical problems such as plumbing and wiring for the first two years, and structural defects for up to 10 years.

Home warranties for existing homes are typically one-year service agreements purchased by buyers or sellers at the time of closing. In the event of a covered defect or breakdown, the warranty firm will step in and make the repair or cover its cost.

Insurance policies and warranties have limitations and individual programs have different levels of coverage, deductibles and costs. For details, speak with us, or your current insurance broker.

How do you get insurance?

You need to have homeowners insurance and warranty coverage buttoned down and arranged before closing, so speak with us or your insurance broker prior to closing. Be sure to ask about limitations, costs, deductibles and “endorsements” (additional forms of coverage that may be available).

This is where you get the keys to your new house!

The “closing” is where we finalize all the steps along the way to your path to buying your first home. It’s where everyone involved in the process gathers to sign all paperwork: you, us, the seller, the seller’s agent and a real estate attorney. We all literally sit at the same table (called the “closing table”) and “close” out the purchase.

The closing process, which in different parts of the country is also known as “settlement” or “escrow,” is increasingly computerized and automated. In many cases, buyers and sellers don’t need to attend a specific event; signed paperwork can be sent to the closing agent via overnight delivery. But typically most of the parties involved attend.

In practice, closings bring together a variety of parties who are part of the “transaction” process. For example, while the history of property ownership has been checked, it’s possible that the records contain errors, unrecorded claims or flaws in the review itself, thus title insurance is necessary but in Colorado, real estate cannot be transferred without a clear title. At closing, transfer taxes must be paid and other claims must also be settled (including closing costs, legal fees and adjustments). In most transactions, the closing attorney also completes the paperwork needed to record the loan.

RELATED: All About Real Estate Closings – What You Need to Know

What to expect

Settlement or closing is a brief process where all of the necessary paperwork needed to complete the transaction is signed. Closing is typically held in an office setting, sometimes with both buyer and seller at the same table, sometimes with each party completing their papers separately.

Whatever the case, the result is that title to the property is transferred from seller to buyer. The buyer receives the keys and the seller receives payment for the home. From the amount credited to the seller, the closing agent subtracts money to pay off the existing mortgage and other transaction costs. Deeds, loan papers, and other documents are prepared, signed and filed with local property record offices.

RELATED: When Closings Go Wrong

What you need to do

One of the best parts of settlement is that buyers and sellers need to do very little.

Before closing, buyers typically have a final opportunity to walk through the property to assure that its condition has not materially changed since the sale agreement was signed. At closing itself, all papers have been prepared by closing agents, title companies, lenders and lawyers. This paperwork reflects the sale agreement and allows all parties to the transaction to verify their interests. For instance, buyers get the title to the property, lenders have their loans recorded in the public records and state governments collect their transfer taxes.

RELATED: Why the Walk Through Matters for Buyers and Sellers

Congratulations! You’re a homeowner now!

You’ve done it. You’ve looked at properties, made an offer, obtained financing and gone to closing. The home is yours. Is there any more to the home buying process?

Whether you’re a first-time buyer or a repeat buyer, there are several more steps you’ll want to take.

Those papers you received at closing are extremely valuable, so hold on to them! In the short-term they can help establish tax deductions for the year in which the property was purchased. In the future, such papers will be important for tax purposes when the property is sold, and in some cases, for calculating estate taxes.

Before closing we will provide you with the names of the utilities, water, sewage, gas, electric and oil service. You will need to have already contacted utilities to have them transferred to your name on closing day. Usually such transfers can be done without turning off utilities.

About a month after closing, you will receive your recorded deed of your property mailed from the attorney. They will take care of recording. If you haven’t received it after a couple of months, call the closing attorney to see what the status is.

Moving in

It is generally understood that sellers will leave homes “broom clean” when moving out. This expression does not mean “vacuumed” or “spotless.” Broom clean makes sense because it means the house is ready to be painted and cleaned.

RELATED: How to Make Moving as Easy as Possible

RELATED: Protect Yourself Against Moving Fraud

Your home, your money

For most owners a home is the largest single asset they hold, so it makes sense to protect that asset.

Many owners make a photo or video record of the home and their possessions for insurance purposes and then keep the records in a safety deposit box. Your insurance provider can recommend what to photograph and how to secure it.

You have to maintain fire, theft and liability insurance. As the value of your property increases such coverage should also rise. Again, speak with your insurance professional for details.

Lastly, enjoy your first home. Owning real estate involves contracts, loans, and taxes. You’ve worked hard to get it. But ultimately what’s most important is that home ownership should be a wonderful experience. Enjoy!

We realize this seems like a lot, but we’re on your side every step of the way. It’s our job to get you through this process as smoothly as possible: Your Dreams. Our Mission. Don’t hesitate to ask us any question or express any concerns.

YOU HAVE QUESTIONS, WE HAVE ANSWERS.

Answering your home buying questions is precisely what we’re here for! We’re happy to answer your questions anytime via phone, text, or email, but we’ve also decided to tackle some of the most common buyer questions right here.

Below, we’ve listed some of the most frequently asked questions, or F.A.Q.’s, that we get asked by our home buying clients. Just click each question to expand the text and see the answer:

It’s more than just a pretty face.

When you visit a property, take note of more than the paint colors. Make a note of the following-Floor plans/layout, strange smells/musty odors can indicate mold, cracks in the basement or foundation, signs of uneven settling, buckling shingles/old roof, drainage in the yard or pooling water, moisture damage on siding, ceilings or walls. But ask us as we’ve experienced many, many more issues with homes.

Being pre-qualified opens all the doors you want.

There’s more to buying a house than most people think! This important first step will make sure you are prepared for the home buying process.

- Understanding the home buying process/approval for mortgage process.

- What banks look for on your application and what you can afford.

- Pre-approved buyers are serious about making a purchase and sellers will respond faster to pre-approved buyers, than someone who has not been pre-approved.

- A pre-approval saves time when putting together an offer, as it must be submitted with the offer.

- Cash deals also require a proof of funds letter, must be submitted at the time of the offer.

READY TO GET STARTED?

We want to show you how the Realtor you choose to work with can make a BIG difference in your home buying experience.

From showings and contracts to inspections and negotiations, we’ve got you covered!

POPULAR BLOG POSTS

5 Great Reasons Why Buying a Home During the Winter Makes Sense

Are you thinking about buying a home on the Western Slope of Colorado? You might wonder if winter is the right time. It turns out, winter might just be the perfect season to find your cozy dream home. Here are five great reasons why winter is a smart time for buying a home in places [...]

5 Tips for Getting the Best Home Buying Deal During a Seller’s Market on the Western Slope of Colorado

Photo by Andrea Piacquadio: https://www.pexels.com/photo/crop-businessman-giving-contract-to-woman-to-sign-3760067/ If you're looking to buy a home on the Western Slope of Colorado, you may have noticed that it's currently a seller's market. That means there are more buyers than there are available homes, and home sellers are in a position of power. But don't let [...]

Homebuyers Beware: Top 3 Things That Could Cause You to LOSE YOUR DEPOSIT!

An earnest money deposit is substantial, so buyers should know what will cause their money to be forfeited, and how to avoid (or leverage!) those instances.

SUBSCRIBE TO THE BLOG FOR WEEKLY UPDATES!

SUBSCRIBE TO THE WEEKLY BLOG!

If you enjoy the content we post weekly, subscribe to our blog! We have a strict NO SPAM guarantee, and we promise valuable information for homeowners (or future homeowners!) in Grand Junction, Clifton, Fruitvale and the surrounding areas.

LATEST BLOG POSTS

The Most Expensive Words You’ll Read While Buying a Home

Sometimes the biggest red flag isn't what you see — it's what you don't hear. Buying a home is exciting. You scroll through the photos. The kitchen looks amazing. The backyard is perfect. The living room has exactly the look you've been hoping for. Then you schedule a showing. But before you do, there's one [...]

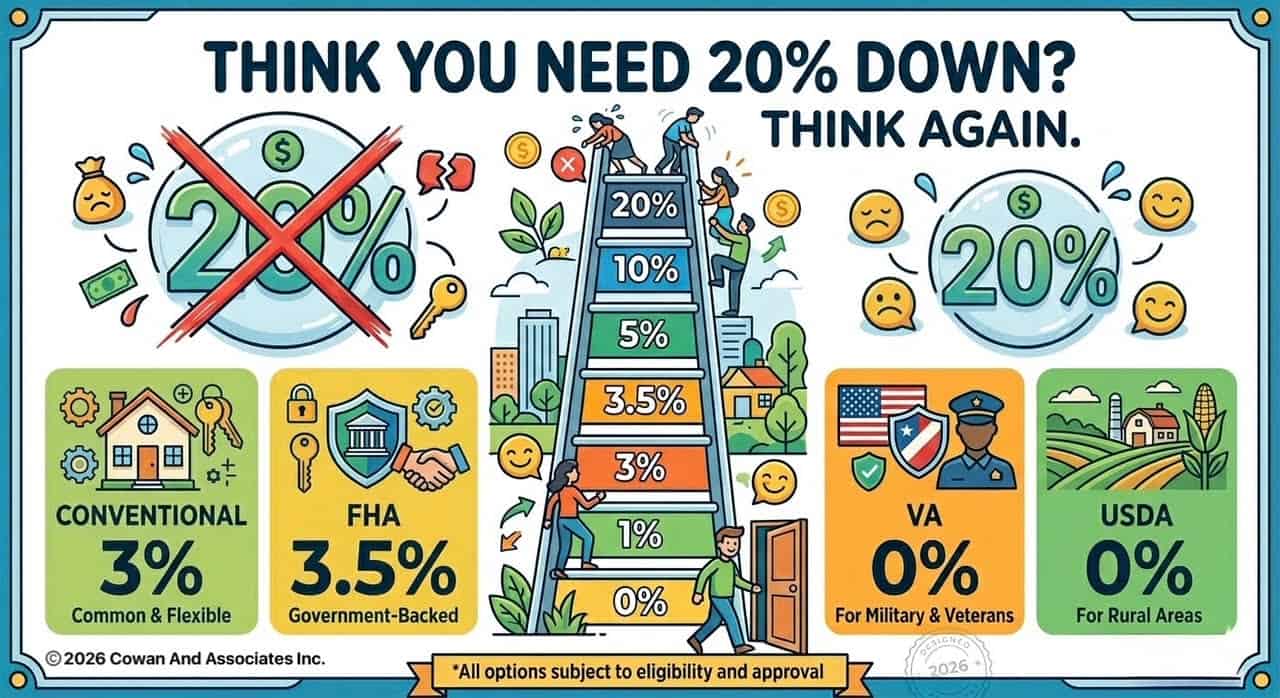

The 20% down payment rule is mostly a myth. Many programs let you buy with less

The 20 percent down payment is still one of the most stubborn myths in real estate, lingering in the minds of many buyers even as financing options have evolved. 🏡 Most first-time buyers and those relocating to Western Colorado discover the reality is much different once they dig into their options. Programs exist that make [...]

Upsizing in Delta, Colorado

Thinking about buying a bigger home in Delta, Colorado? If you're looking to upsize, you're not alone. Many families find themselves needing more space — whether it's for growing kids, a home office, or extra room for guests. However, buying a larger home comes with its own set of challenges. Here's what you need to [...]